You knew there had to be a catch, and here it is: Because an FHA loan does not have the strict standards of a conventional loan, it requires two kinds of mortgage insurance premiums: one is paid in full upfront – or, it can be financed into the mortgage – and the other is a monthly payment. Also, FHA loans require that the house meet certain conditions and must be appraised by an FHA-approved appraiser.

Upfront mortgage insurance premium (MIP) — Appropriately named, this is an upfront monthly premium payment, which means borrowers will pay a premium of 1.75% of the home loan, regardless of their credit score. Example: $300,000 loan x 1.75% = $5,250. This sum can be paid upfront at closing as part of the settlement charges or can be rolled into the mortgage.

Annual MIP (charged monthly) —Called an annual premium, this is actually a monthly charge that will be figured into your mortgage payment. It is based on a borrower's loan-to-value (LTV) ratio, loan size, and length of loan. There are different Annual MIP values for loans with a term greater than 15 years and loans with a term of less than or equal to 15 years. Loans with a term of greater than 15 Years and Loan amount < or =$625,000.

- Loans with a term of greater than 15 Years and Loan amount < or =$625,000

- LTV less than or equal to 95 percent, annual premiums are 1.30%

- LTV above 95 percent, annual premiums are 1.35%.

- Loans with a term of greater than 15 Years and Loan Amount >$625,000

- LTV less than or equal to 95 percent, annual premiums are 1.50%

- LTV above 95 percent, annual premiums are 1.55%

- Loans with a term of 15 years or less and Loan amount < or =$625,000

- LTV less than or equal to 90 percent, annual premiums are .45%

- LTV above 90 percent, annual premiums are .70%

- Loans with a term of 15 Years or less and Loan Amount >$625,000

- LTV less than or equal to 90 percent, annual premiums are .70%

- LTV above 90 percent, annual premiums are .95%

Example (for LTV less than 95 percent on a 30 year loan): $300,000 loan x 1.30% = $3,900. Then, divide $3,900 by 12 months = $325. Your monthly premium is $325 per month. The Mortgage Insurance will be in your payments for the entire loan term if your LTV is >90%. If your LTV is = or < 90%, the Mortgage Premium will be for the mortgage term or 11 years, whichever occurs first.

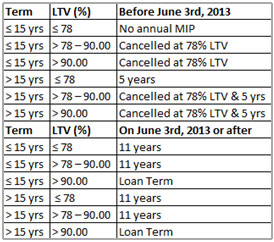

Single family home mortgages with amortization terms of 15 years or less, and a loan-to-value (LTV) ratio of 78 percent or less, remain exempt from the annual MIP.

FHA Mortgage Insurance Duration

The duration of your annual MIP will depend on the amortization term and LTV ratio on your loan origination date. Please refer to this chart for more information:

When choosing the right mortgage for your home purchase, there are many different things to consider. While an FHA mortgage does have an insurance requirement, it can also provide an affordable option for individuals and families looking to purchase their first home or refinance their current home.

Our team can walk you through the MIP process, helping you to determine how much it will cost you throughout the life of your home mortgage loan. Plus, we can walk you through the rest of the loan terms to better understand your costs, both at closing and monthly. This can effectively help you manage your budget, regardless of the economic climate.